Jun 04, 2026 · By Aura ETFs

The Global Rearmament Cycle: What Defense Investors Need to Know

Key Takeaways:

- Backlogs are large, but they reflect both strength and strain: Record backlogs across major prime contractors show strong demand and long-term revenue visibility.

- The cycle is measured in years, not quarters: Between backlog conversion, stockpile rebuilding, and industrial expansion, the current defense cycle is likely to unfold over a longer time horizon than typical market narratives suggest.

- High-consumption warfare is changing procurement patterns: Artillery shells, missile interceptors, and drones are being used at rates that exceed pre-war planning assumptions. This shifts defense spending toward recurring demand rather than one-time platform purchases.

The post-Cold War “peace dividend” has given way to a more fragmented security environment, and global defense spending is entering a new phase of sustained growth.

Rising geopolitical tensions, including the ongoing war in Ukraine and escalating conflicts in the Middle East, have pushed governments to reassess military readiness and rebuild depleted capabilities.

Modern conflicts are consuming equipment at a faster pace than expected, particularly in areas like munitions, air defense systems, and drones. Replenishing these stockpiles and expanding production capacity may take years, creating a more durable demand backdrop.

In this whitepaper, we explore the key drivers behind today’s rearmament cycle, how defense stocks have historically responded to conflict, and where new opportunities may be emerging. The goal is to provide a practical framework for understanding how defense investing is evolving and how to allocate.

A structural shift: global defense spending acceleration

Global defense spending is moving through a clear structural reset. What was once a baseline target is now being treated as a minimum requirement, with governments revising long-term commitments upward in response to a more uncertain security environment.

For much of the past decade, NATO’s 2% of GDP defense spending target served as a benchmark that many members struggled to meet. That framework is now being redefined.

At the 2025 NATO summit in The Hague, member countries committed to significantly higher levels of investment, targeting 5% of GDP in total defense-related spending. This includes 3.5% allocated to core military expenditures and an additional 1.5% directed toward areas such as critical infrastructure, cyber defense, and civil preparedness.

The scale of this increase marks a decisive break from the post-2014 framework and reflects a broader recognition that prior spending levels were insufficient for current threats1. This shift is closely tied to changes in U.S. policy and positioning. The re-election of Donald Trump has reinforced a more protectionist and selective approach to global defense commitments.

U.S. leadership has repeatedly emphasized burden sharing within NATO, pointing out that America continues to account for a disproportionate share of total alliance spending. This has added pressure on European allies to accelerate their own defense budgets and reduce reliance on U.S. support.

Europe has responded with coordinated, large-scale initiatives. The European Union’s “REARM Europe” plan, also referred to as Readiness 2030, outlines over €800 billion in defense-related spending aimed at strengthening regional capabilities.

The bloc also introduced a €150 billion loan facility under the Security Action for Europe (SAFE) framework, designed to support joint procurement and improve coordination across member states. These efforts are being driven in large part by Russia’s ongoing war in Ukraine, now in its fourth year, as well as heightened military activity along NATO’s eastern flank, including in Estonia, Latvia, and Finland.2

Within the United States, the policy response has been equally direct. The 2026 National Defense Strategy outlines four primary lines of effort: defending the homeland, deterring China in the Indo-Pacific, strengthening burden sharing with allies, and expanding the U.S. defense industrial base.

The final point is particularly relevant for investors. The strategy places a clear emphasis on scaling production capacity, strengthening domestic supply chains, and integrating nontraditional vendors alongside established defense contractors.3

“As the NSS makes clear, this effort will require nothing short of a national mobilization—a call to industrial arms on par with similar revivals of the last century that ultimately powered our nation to victory in the world wars and the Cold War that followed.”

Taken together, these developments point to a longer-duration investment cycle. Defense budgets are rising across multiple regions, supported by formal commitments, coordinated funding programs, and multi-year procurement plans. For investors, this creates a more durable and visible demand backdrop

The backlog story: visibility, durability, and constraints

A backlog represents the total value of contracted work that has been awarded but not yet delivered or recognized as revenue. It is future business that is already booked. This is one of the defining features of the defense sector and a key reason it behaves differently from other areas of industrials.

In most cyclical industries such as manufacturing, transportation, or business services, demand can shift quickly with economic conditions. Orders rise and fall, and revenue visibility is often limited to a few quarters. Defense is structured differently.

Contracts are typically long term, funded by governments, and tied to national security priorities rather than consumer demand. This creates a level of forward revenue visibility that is uncommon in other sectors, often extending several years into the future.

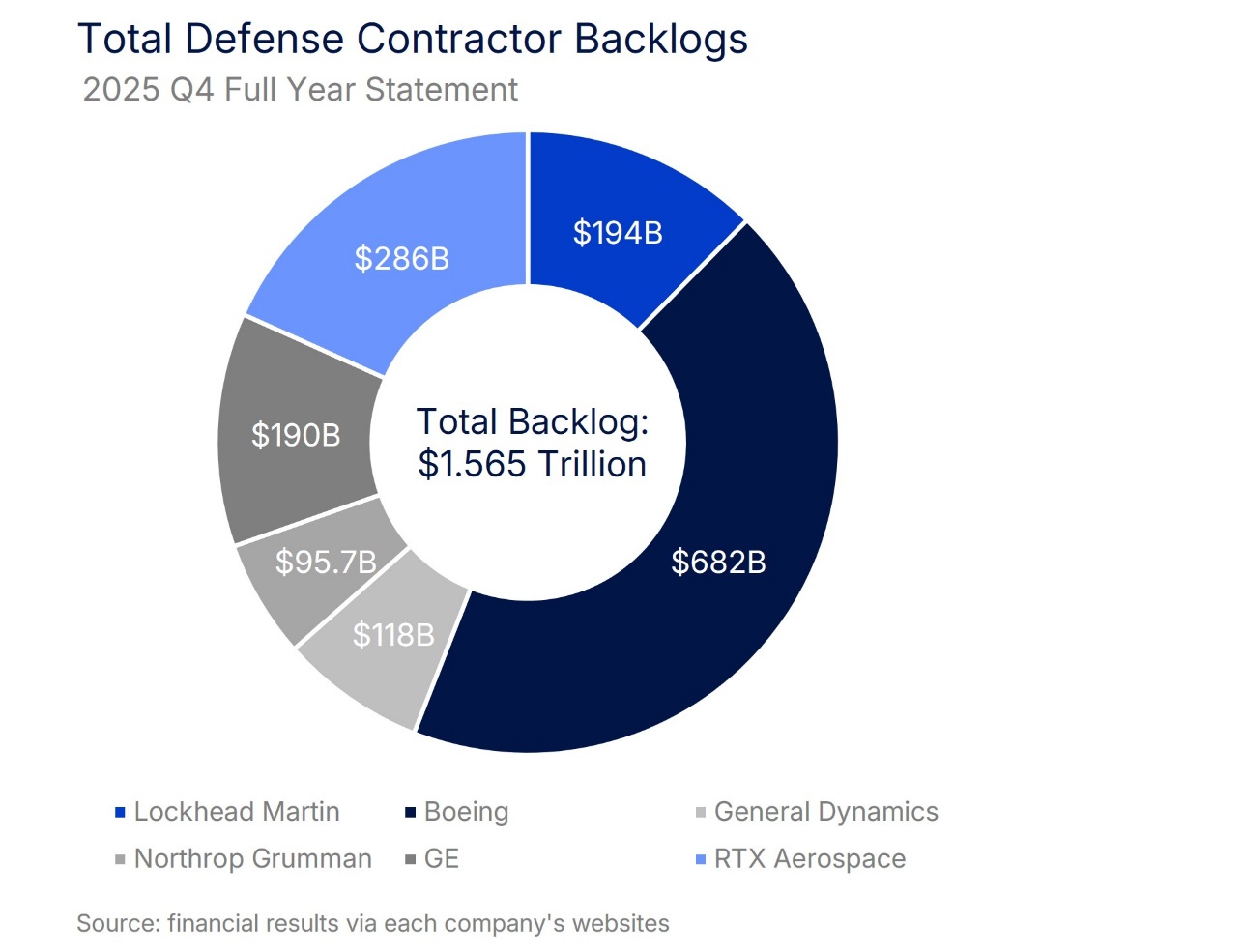

Nowhere is this more visible than among the major prime contractors. As of their latest fourth quarter 2025 and full-year disclosures, backlogs were significant:

These figures highlight the scale and durability of demand. In many cases, backlogs even exceed the companies’ current market capitalizations!

This has important implications for how investors think about valuation. A large portion of future revenue is already contracted, which can support earnings visibility and justify higher multiples in certain environments. At the same time, backlogs are not uniformly positive.

On one hand, a growing backlog signals strong demand, successful contract wins, and long-term revenue support. On the other hand, it can also reflect an inability to deliver. If production capacity is constrained, a rising backlog may indicate that orders are accumulating faster than they can be fulfilled

Conflict-driven demand: munitions depletion and replenishment cycles

Defense manufacturing is not built around a just-in-time model in the way many civilian industries are. Militaries cannot afford to wait until a crisis begins to start placing orders for missiles, artillery shells, interceptors, armored vehicles, or drone systems.

Stockpiles matter because wars do not unfold on predictable production schedules. Once those stockpiles are drawn down, replenishment can take years.

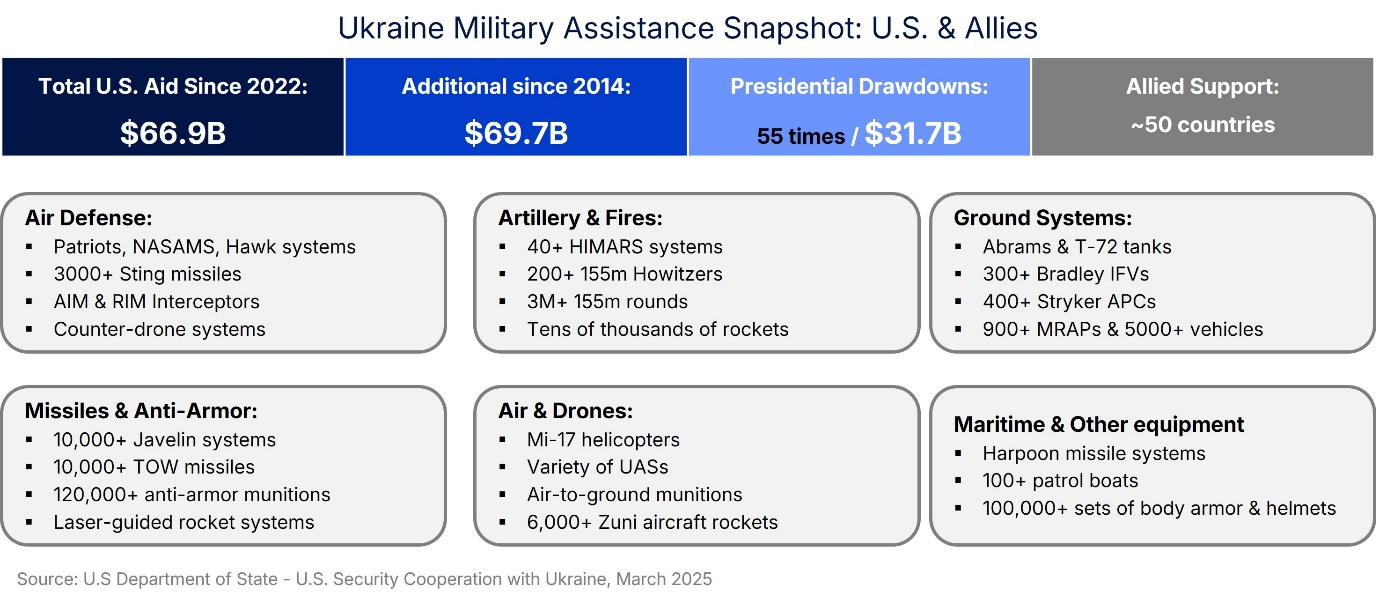

That reality has been on full display during the war in Ukraine. Over four years of sustained, high-intensity conflict, the United States and its allies have transferred enormous volumes of military equipment and ammunition to support Ukraine’s defense.

According to the State Department, the U.S. has provided $66.9 billion in military assistance since Russia’s full-scale invasion in 2022, in addition to $69.7 billion since the initial onset of conflict in 2014. Since August 2021, the White House has used presidential drawdown authority on 55 occasions to provide $31.7 billion worth of equipment directly from Department of Defense stockpiles.

The scale of those transfers helps explain why replenishment has become such a major investment theme. The equipment sent to Ukraine has spanned nearly every major category of modern warfare. Congress has also approved billions more in military financing, while the Department of Defense continued to allocate significant amounts of security assistance through its own budget authorities.4

Modern war consumes materiel at a pace that peacetime procurement planning often underestimates. Artillery shells, interceptors, fighter jets, guided rockets, loitering munitions, and drones are recurring consumables. That challenge is now being compounded by the Middle East.

The escalation involving Israel and Iran has added another layer of demand for air defense interceptors, missile defense systems, tactical aircraft support, and replenishment of precision munitions. Patriot interceptors, terminal missile defense assets, naval missile systems, and counter-drone technologies are all finite resources, and production is not infinitely scalable in the short term.

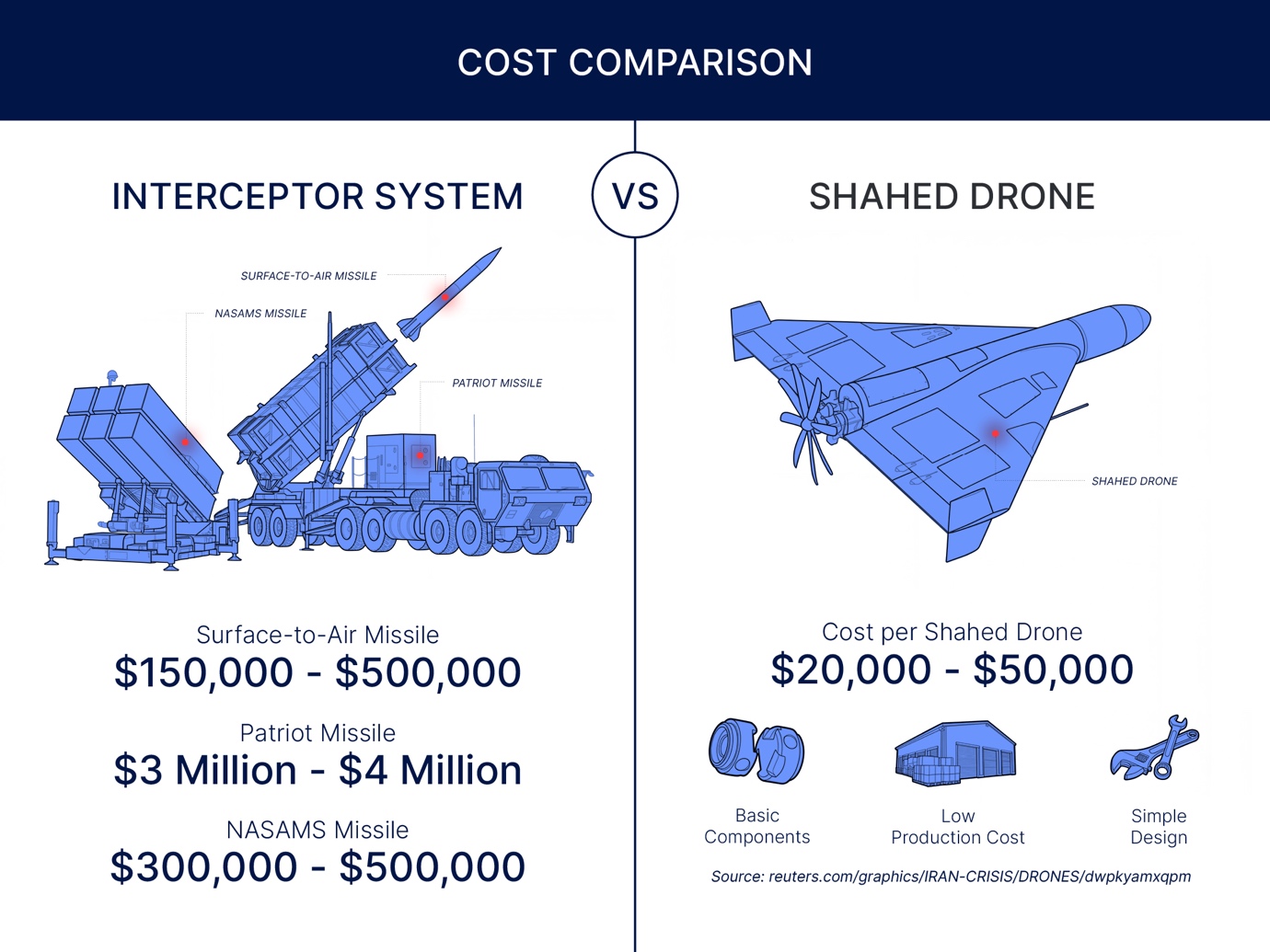

This creates a particularly difficult form of asymmetry for Western militaries. Low-cost one-way attack drones like the Iranian Shahed and other attrition-based systems can be fielded relatively cheaply, while the interceptors used to stop them are often far more expensive and slower to replace.5

Defending against large volumes of low-cost aerial threats can quickly become a costly and inventory-intensive exercise. That drives urgency not only for replenishment of existing missile inventories, but also for investment in directed energy and next-generation drone defense technologies.

This is where the replenishment cycle feeds directly back into the backlog cycle discussed earlier. Governments are accelerating orders, but the Western defense industrial base was not designed for years of sustained, high-intensity, multi-theater demand.

Factories built for peacetime efficiency are now being asked to support wartime consumption rates. Production lines for shells, interceptors, propulsion systems, and advanced munitions are being expanded, but capacity additions take time. New tooling, workforce training, regulatory approvals, and supply chain coordination all slow the process.

For investors, that means conflict-driven demand is not simply a short-term headline catalyst. It can translate into multi-year procurement waves, stockpile rebuilding programs, and expanded capital spending across the defense supply chain.

Related ETFs:

Related Insights

Sources:

- https://www.nato.int/en/what-we-do/introduction-to-nato/defence-expenditures-and-natos-5-commitment

- https://www.europarl.europa.eu/RegData/etudes/BRIE/2025/769566/EPRS_BRI(2025)769566_EN.pdf

- https://media.defense.gov/2026/Jan/23/2003864773/-1/-1/0/2026-NATIONAL-DEFENSE-STRATEGY.PDF

- https://www.state.gov/bureau-of-political-military-affairs/releases/2025/01/u-s-security-cooperation-with-ukraine

- https://www.theatlantic.com/ideas/2026/03/us-iran-war-air-strikes/686228/