May 28, 2026 · By Aura ETFs

The Strategic Case for U.S. Defense Sector Investing

Key Takeaways

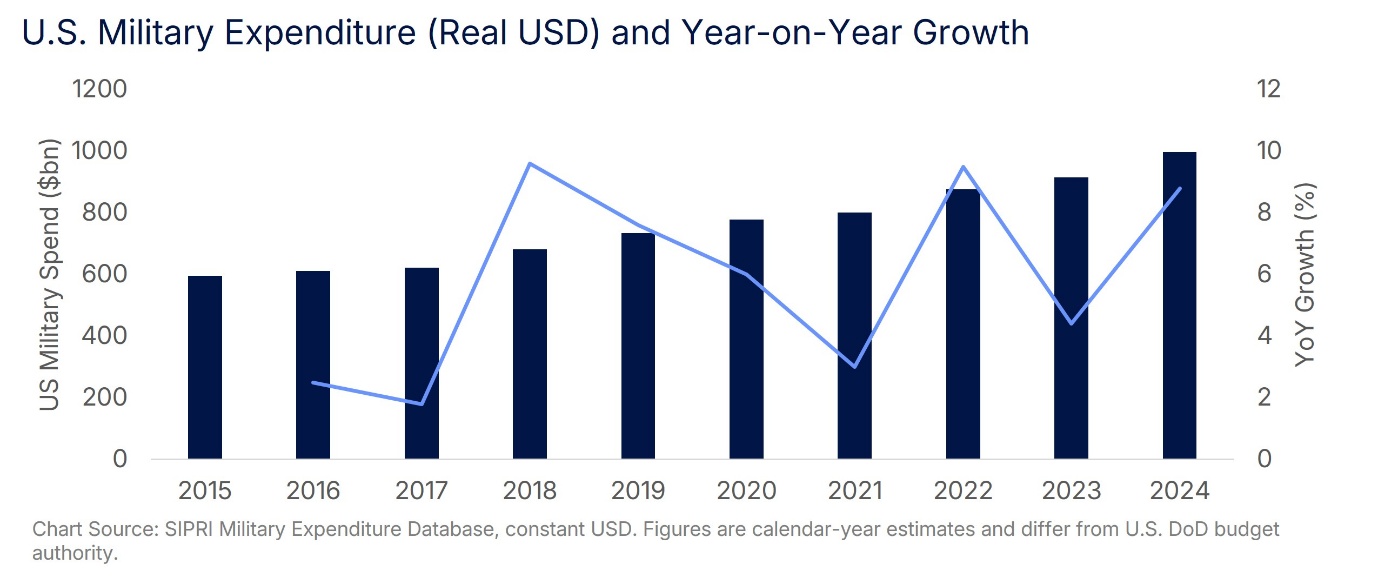

- The United States spent roughly $997 billion in 2024, representing about 37% of global spending and ~66% of NATO member spending.¹

Major defense contractors. maintain multi-year order backlogs, often exceeding annual revenue, reflecting long-cycle demand visibility.2

- Procurement and R&D spending have increased as modernization accelerates.

- Defense spending is structurally persistent due to alliance commitments, global force posture and technology competition.

U.S. Defense Spending Is Structurally Persistent

Most industries depend on consumer demand or corporate investment cycles. The defense sector is different.

Demand is determined primarily by government budgets, national security priorities and alliance commitments. These drivers evolve slowly and are often independent of short-term economic conditions.

According to Stockholm International Peace Research Institute data, global military expenditure reached roughly $2.7 trillion in 2024, with the United States accounting for approximately $997 billion.¹

This scale reflects the long-term allocation of national resources toward defense.

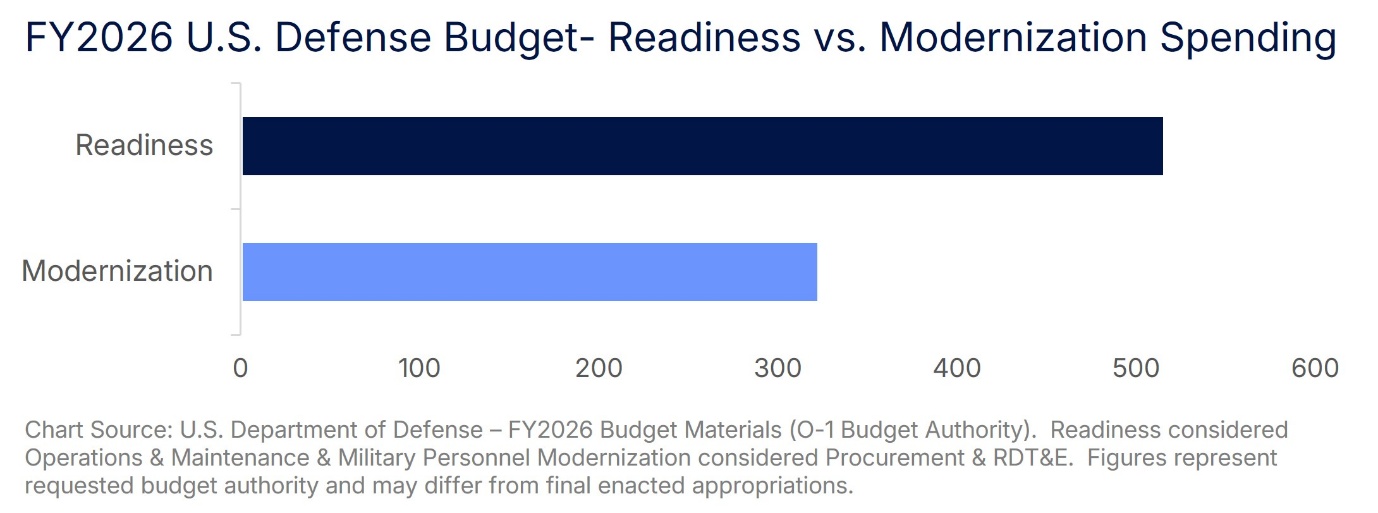

Within that total, the U.S. Department of Defense FY2026 budget request alone is approximately $893 billion, illustrating the size and persistence of Pentagon spending.3

Defense spending has historically remained around 3–5% of U.S. GDP, demonstrating how national security priorities maintain consistent funding levels across decades.

Defense Spending Reflects Global Commitments

The United States maintains hundreds of overseas installations and forward-deployed forces across multiple regions, reflecting global alliance commitments and long-term logistics requirements.

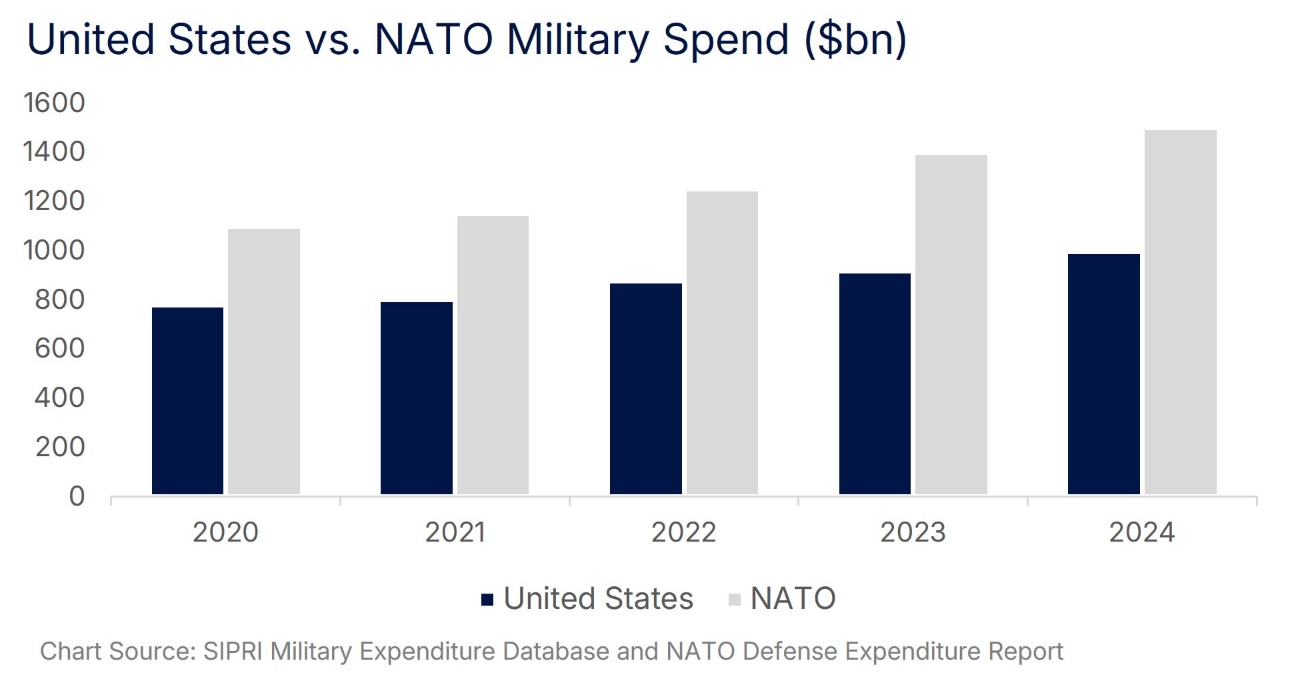

NATO members collectively spent over $1.5 trillion on defense in recent years, with the United States representing roughly two-thirds (66%) of NATO defense spending.¹

Maintaining alliance credibility requires funded readiness, logistics infrastructure and global force posture.

Personnel, operations and sustainment costs therefore continue even during economic slowdowns. This helps explain why defense budgets tend to persist across cycles.

These commitments also influence procurement programs, as allied interoperability requirements drive investment in aircraft, naval systems, communications networks and munitions.

Modernization Is Changing Budget Composition

Modern defense priorities increasingly emphasize advanced technology.

According to FY2026 DoD budget materials, the request was approximately $893 billion split; Operations & Maintenance ~37%, Military Personnel ~21%, Procurement ~20%, and Research, Development, Test & Evaluation (RDT&E) ~17%.3

These categories illustrate how resources are split between readiness today and modernization for the future.

Procurement funds aircraft, ships, submarines, vehicles, missiles and communications systems. RDT&E supports technologies such as cyber defense, autonomous systems, advanced sensors and space-based communications.

Because research programs often lead to procurement programs years later, sustained RDT&E spending creates long-term demand across the defense industrial base.

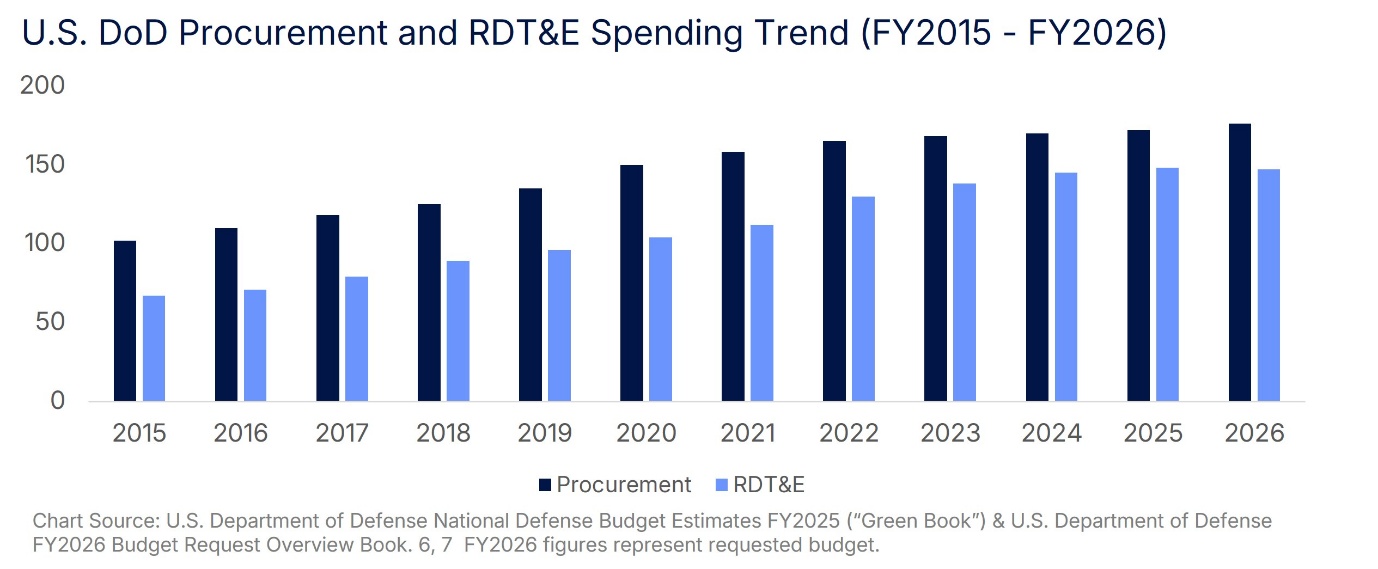

DoD historical budget tables show procurement rising from roughly $102 billion in FY2015 to about $170 billion in FY2024, with the FY2026 request of approximately $176 billion continuing this modernization trend.3

RDT&E spending has also increased materially over the past decade, reflecting growing investment in advanced technologies.

What Procurement Spending Buys

Procurement spending provides the clearest view of how defense budgets translate into industrial activity. Defense companies operate under multi-year procurement programs and regulated contracting frameworks. Security clearances, export controls and specialized engineering requirements create high barriers to entry.

Once a company is integrated into a defense program, contracts may continue for many years. This creates backlog visibility.

Recent filings show major contractor backlogs such as: Lockheed Martin (~$195bn), RTX Corp (~$268bn), Northrop Grumman (~$84bn) and L3Harris Technologies (~$34bn).2 These backlogs often exceed annual revenue, indicating demand visibility across multiple years.

Backlog represents contracted orders and is not a guarantee of future revenue, but it is a useful indicator of the scale and duration of funded programs. It also highlights how defense spending is translated into multi-year production schedules and sustainment activities across a broad supplier base.

Major procurement programs such as the F-35 fighter aircraft, Virginia-class submarines and Columbia-class ballistic missile submarines involve multi-decade development, production and sustainment cycles that extend demand across prime contractors, suppliers and service providers.4

Defense Spending Flows Across Many Industries

The defense sector includes more than aircraft or ship manufacturers. It also includes companies providing cybersecurity and digital infrastructure, electronics and sensor technology, logistics and maintenance services, software and communications platforms, and simulation and training systems.

Modern military systems rely on integrated supply chains combining hardware, software and services. As a result, defense spending supports a wide ecosystem of industries.

For example, aircraft programs rely on electronics suppliers, materials companies, software developers and maintenance contractors. Naval shipbuilding requires propulsion systems, radar manufacturers, communications equipment and logistics support.

Understanding these supply chains is important because different companies may benefit from different parts of the defense budget. A prime contractor may be exposed to production volumes, a supplier may depend on demand across multiple platforms, and a technology provider may benefit from upgrades and integration work.

Barriers to Entry Create Competitive Moats

Defense contracting frameworks require security clearances, regulatory approvals and specialized engineering capabilities. These barriers limit new entrants and help maintain supplier relationships across programs.

Companies often invest heavily in research and development (R&D) to remain competitive. Defense R&D intensity can be higher than in other industrial sectors because advanced capabilities require long lead times, specialized manufacturing and rigorous testing.

Because of these barriers, defense companies can remain embedded in programs for long periods, providing revenue visibility and long customer relationships. At the same time, program complexity can create execution risk, reinforcing the importance of diversified exposure across the defense value chain.

Defense Spending and Economic Cycles

Defense budgets are influenced by national security priorities rather than consumer demand.

Even during economic slowdowns, governments must maintain readiness, personnel and equipment. Procurement programs also continue once contracts are signed, and sustainment spending can persist for decades after platforms enter service.

As a result, defense spending often evolves gradually rather than changing sharply. Individual programs may shift, but overall spending tends to persist because large procurement plans and alliance commitments are built over many years.

This structure differentiates defense companies from highly cyclical industries such as consumer discretionary or housing-related sectors.

How Investors Evaluate the Defense Theme

Investors often approach the defense sector through a combination of macro and micro lenses. At the macro level, the question is whether national security priorities support sustained budget funding over time. At the micro level, the question is how budget allocations translate into revenue streams for different parts of the industrial base, platform primes, subsystem suppliers, software and cyber providers, and services companies.

Because defense is a regulated market with long program lifecycles, many companies can display characteristics that differ from typical industrial cyclicals: multi-year contract visibility, a large proportion of government customers, and recurring sustainment and services revenue once equipment is deployed.

At the same time, investors should recognize that program timing, procurement priorities and contract structures can vary, which is why diversified exposure across the defense value chain is often emphasized in sector allocations.

From an investment perspective, modernization matters because it can change the composition of defense revenue. Shifts toward precision munitions, autonomous platforms, advanced sensors and secure communications can increase demand for electronics, software and integration capabilities alongside traditional manufacturing. Monitoring the balance between procurement and RDT&E, and the categories within procurement, can therefore provide a useful signal of where modernization dollars are flowing.

Conclusion

The strategic case for investing in the U.S. defense sector rests on three structural factors: (1) the scale of global and U.S. defense spending, (2) long-cycle procurement and backlog visibility, and (3) technology-driven modernization.

This framework is particularly relevant for thematic ETFs that seek exposure to companies across the defense value chain.

Defense spending reflects national security priorities that evolve over long horizons, and procurement and research programs support a wide range of industries, from aerospace and shipbuilding to cybersecurity and advanced electronics.

For investors, understanding these structural drivers helps explain why exposure to the U.S. defense sector is often viewed as a long-term thematic allocation.

Related ETFs:

Related Insights

Sources:

- SIPRI Fact Sheet – Trends in World Military Expenditure 2024: https://www.sipri.org/sites/default/files/2025-04/2504_fs_milex_2024.pdf

- Company Annual Reports and SEC Filings: https://www.sec.gov/edgar/search/: Lockheed Martin – Form-10K Dec 2025, RTX Corp – Form-10K Dec 2025, Northrop Grumman – Form-10K Dec 2025, L3Harris Technologies – Form-10K Dec 2025

- U.S. Department of Defense – FY2026 Budget Materials: https://comptroller.defense.gov/Budget-Materials/Budget2026/

- U.S. Government Accountability Office - Weapon Systems Annual Assessment: https://www.gao.gov/assets/gao-24-106831.pdf